Online Account Opening

When you've got big plans for your business, you want a bank you can rely on.

Find out moreFINANCIAL SUPPLY CHAIN MANAGEMENT

SUSTAINABLE TRADE FINANCE

Johor-Singapore SEZ

Integrates two economies into one ecosystem, unlocking new levels of collaboration

Find out more

UOB Sustainability Compass

Your go-to sustainability guide. Get your customised report today by taking the quiz now.

Take the quiz-

you are in WHOLESALE BANKING

For Individuals

Personal BankingWealth BankingPrivilege BankingPrivate BankUOB ReferralFor Companies

Foreign Direct InvestmentUOB ASEAN InsightsIndustry InsightsUOB Islamic Banking

Islamic BankingAbout UOB

Corporate ProfileStakeholder RelationsUOB Digitalisation

What is it?

A Cross Currency Swap (CCS) is an instrument which allows two parties to exchange a series of cashflows from one currency to another based on contracted rates. Using a CCS, you can synthetically swap a currency exposure of your asset or liability to another effectively.

Key uses

The primary use of a Cross Currency Swap is the ability to synthetically swap one currency exposure to another. For example, if a company is only able to borrow MYR but requires a loan in USD, he can use a CCS to swap the MYR loan into a USD loan. The ability of a Cross Currency Swap to synthetically transform the currency exposure of an underlying asset or liability provides an effective way to hedge currency risk, as well as to access foreign currency funding sources if favourable.

Benefits

Manage currency mismatches

Effectively manage foreign currency risks from foreign currency loans and assets.

Mitigate interest rate risks

Protect against interest rate risks by electing to pay a fixed coupon in the CCS.

Optimise funding sources

Leverage your funding strength in one currency for use in another currency.

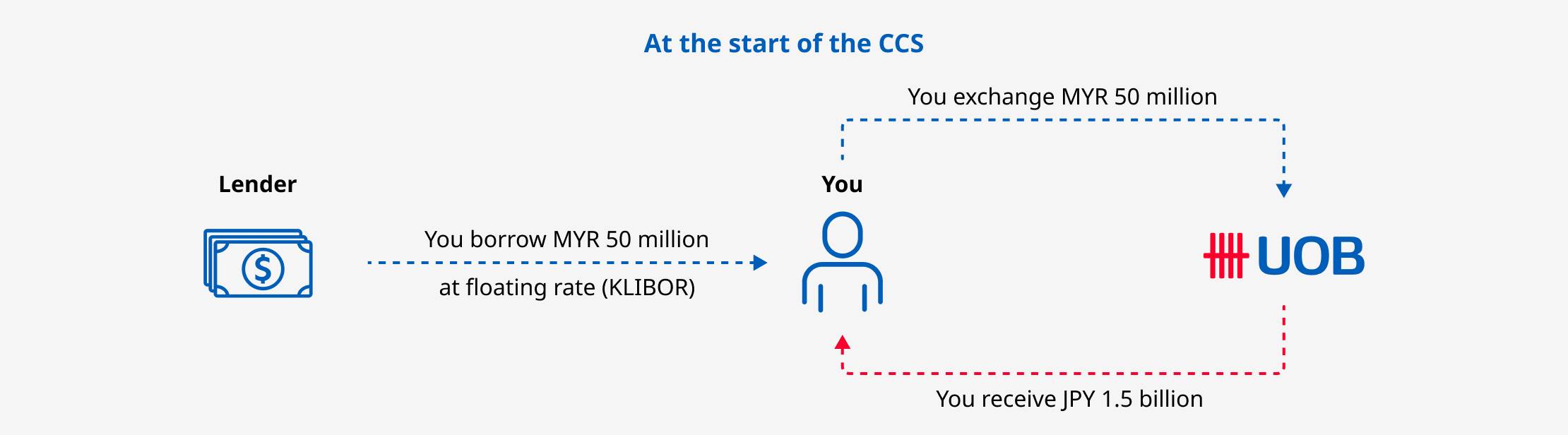

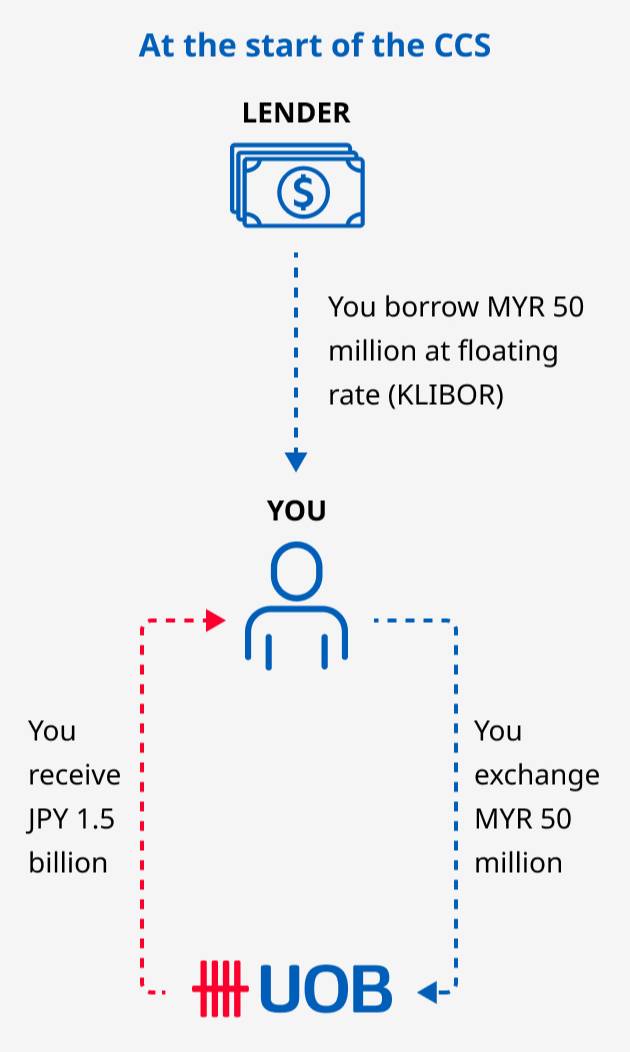

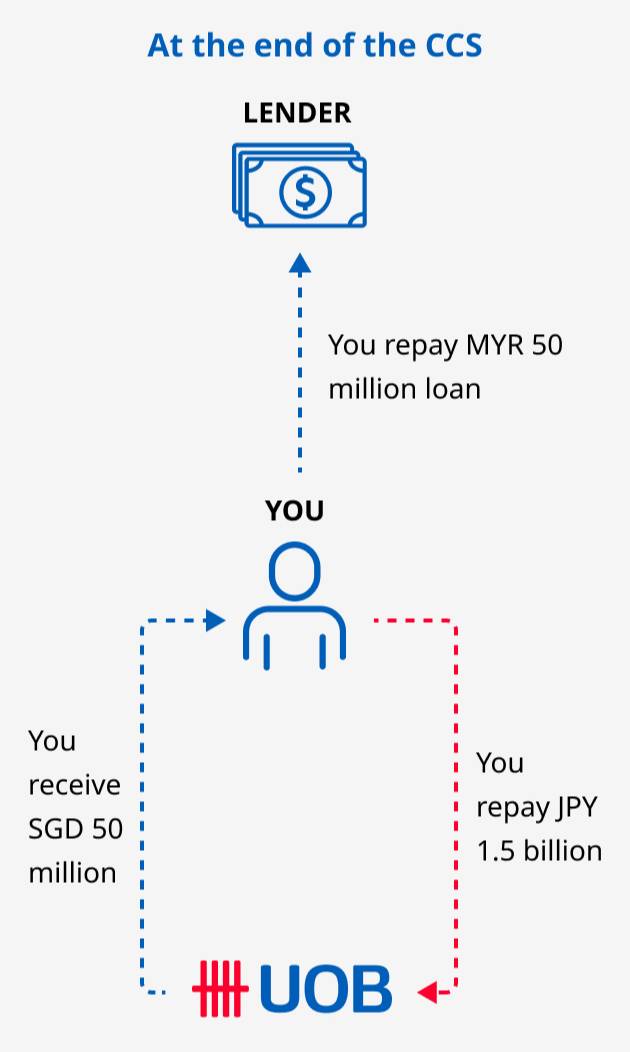

Scenario

Your company has a loan of MYR 50 million on a floating interest rate (i.e. MYR KLIBOR). You would like to execute a Cross Currency Swap to transform your loan into a Japanese Yen denominated fixed interest rate loan.

How it works: On the start date, your company will receive MYR 50 million from your lender. Your company can then exchange the MYR 50 million into Japanese Yen at a predetermined foreign exchange rate using a CCS.

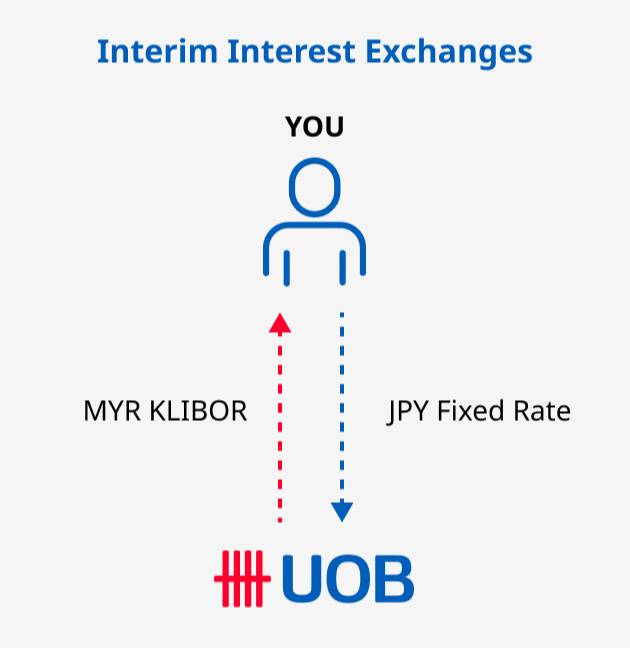

How it works: During the interim, your company will receive MYR KLIBOR floating interest rate which will match your loan’s interest rate payments. In exchange, your company will pay JPY fixed rate to UOB.

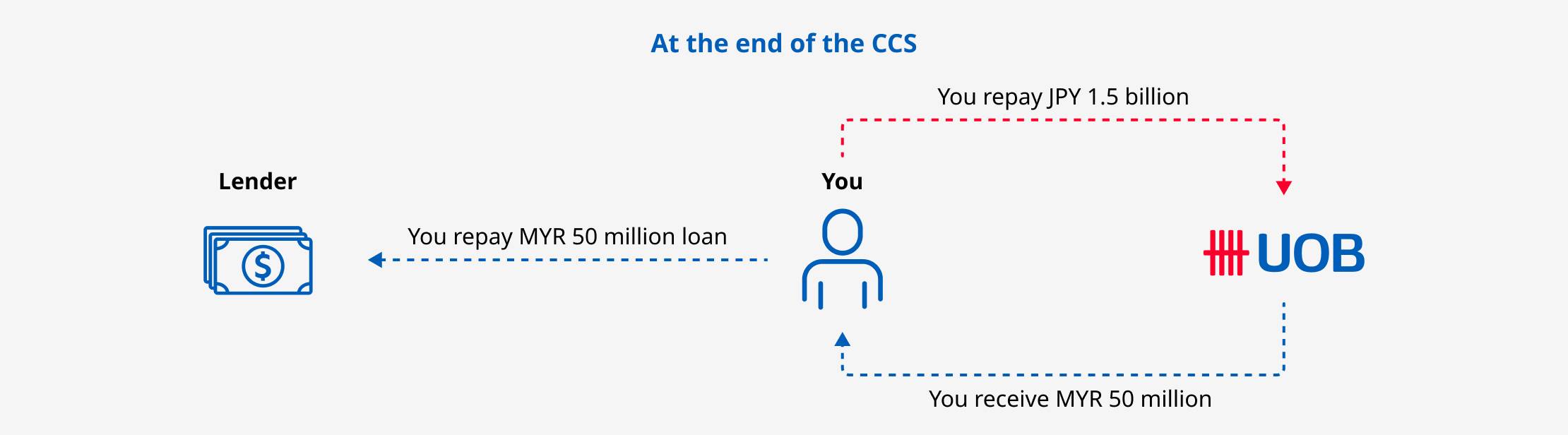

How it works: At maturity, your company will exchange the JPY 1.5 billion back into Malaysian Ringgit at the same exchange rate used at the start of the CCS. With the MYR 50 million received from UOB, your company will use it to repay its existing loan.

Disclaimer: This is only an illustration, it does not constitute an offer or an invitation to offer or a solicitation or recommendation to enter into or conclude any transaction. Please contact UOB for more information.

You may also like

Interest Rate Swap

Hedge your loan against interest rate risks.

Currency Hedging (FX)

Trade with confidence by leveraging on our competitive rates and dedicated services.

Commodity Hedging

Leverage on our highly experienced team to manage and mitigate the risk of fluctuation in commodity prices.

We're here to help

We use cookies in order to provide you with better services on our website. By continuing to browse the site, you agree to our privacy notice and cookie policy.