You are now reading:

SME cash flow woes? 5 ways to help your small business survive

When you've got big plans for your business, you want a bank you can rely on.

Find out more

Integrates two economies into one ecosystem, unlocking new levels of collaboration

Find out more

Your go-to sustainability guide. Get your customised report today by taking the quiz now.

Take the quizyou are in WHOLESALE BANKING![]()

You are now reading:

SME cash flow woes? 5 ways to help your small business survive

SMEs are an essential component of the economy, making up 98.5 per cent of business entities in Malaysia. In 2019, SMEs contributed 38.9 per cent to the country's GDP, 66.2 per cent of the workforce and 17.3 per cent of exports, according to SME Corp Malaysia's 2018-19 Annual Report.

The COVID-19 pandemic is an unforeseen global phenomenon which has thrown the economy into chaos and effectively put commerce at a standstill. It has unilaterally affected most businesses.

Even at the best of times, SMEs keep a close eye on their cash flow. It is, after all, the lifeblood of their business. But in today’s environment, with both consumers and businesses reeling from the impact of the pandemic, managing cash flow has never been more important.

Here are 5 ways to help your small business survive during this challenging phase.

Most small businesses are intimately familiar with the scourge that is late invoice payments. While a lot of it is out of your control (your customer may be facing cash-flow difficulties of their own, for instance), one part is 100 per cent up to you: invoicing on time. Even with a late-paying customer, invoicing late gives them an excuse to pay you even later, placing further strain on your cash flow.

The lesson: keep close track of your invoices and always send them out on time. The same also applies to businesses that stock inventory. Inventory costs cash, and many cash flow issues can be traced back to poor inventory management.

Of course, most businesses know this. The issue is establishing an easy-to-use system that allows you to track invoices and inventory – and one that does not eat away at your already-busy schedule.

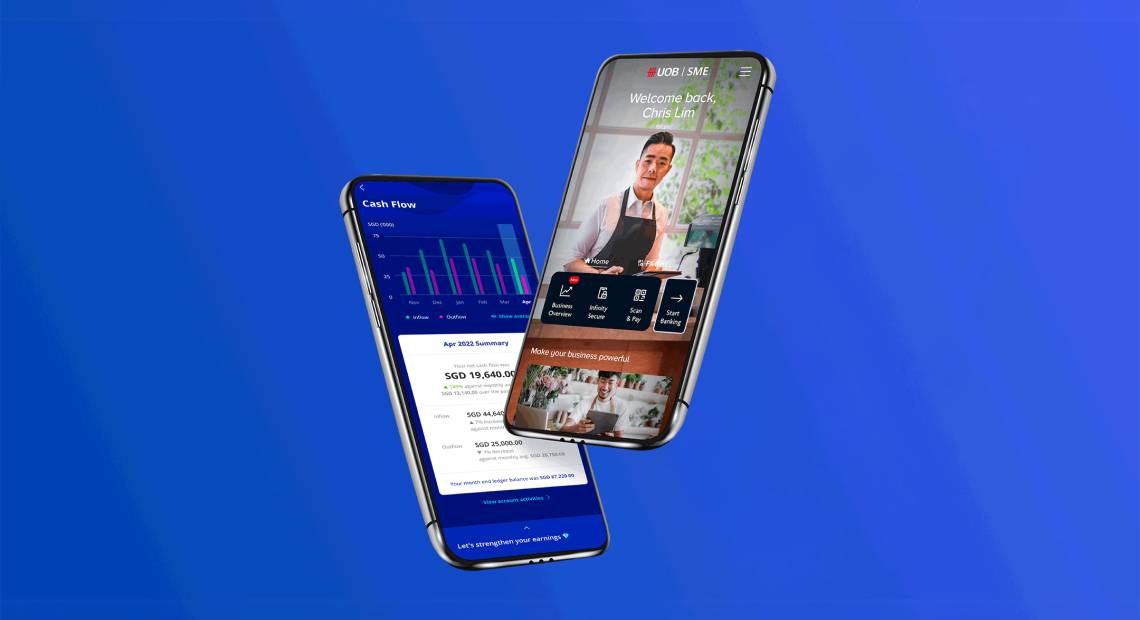

UOB SmartBusiness was developed to tailor to these needs. It offers a suite of integrated solutions that lets you seamlessly manage multiple core processes such as sales, invoicing, payroll, accounting and more. This ready access to your financials allows you to make better-informed business decisions and generate better cash flow.

Most businesses think of their operating account as nothing more than a mere necessity. They use it for receiving customer payments and disbursing funds to suppliers, staff, and the like. But while that is no doubt its primary use, did you know that you can also use it to help improve your cash flow?

If you have a high transaction volume, for instance, expensive clearing and transaction fees can quickly add up. And if you have high average balances, letting it sit there without earning interest is costing you real money.

At UOB, we offer BizCA+, to help businesses capture all these 'small wins' so they can compound into big wins. Along with attractive interest rates with no lock-in period, BizCA+ account holders can perform unlimited transactions via BIBPlus for Interbank GIRO, DuitNow, and RENTAS for free.

Negotiation is one of the most valuable business skills – and for a good reason. While important during prosperous times, they become vital in a cash flow-pressured environment.

Two ideas to consider: requiring deposits on large orders from customers, and staggering payments on long-term contracts with vendors. The former helps reduce the 'counterparty risk' of the customer, while the latter lets you keep more cash in your account (instead of your suppliers). Both will improve your cash flow.

The caveat, of course, is you need to ask for these terms and be prepared to negotiate. Prepare yourself by studying the relationship you have with your customers and suppliers to understand the leverage you have (for example, your credit history with a supplier). Use that as the base for your negotiation approach.

In a nutshell, invoices are assets of a company. The product or service has been completed and delivered, but the cash is locked up in the invoice until the customer pays. External financing solutions like invoice financing offers a way for businesses to free up capital that would otherwise be tied up in outstanding invoices for 30 days or longer. You could obtain funding as soon as within a day or two from your application - which makes this a great option if you require immediate financing.

To help businesses get through this challenging time, both banks and the government have stepped in to help. UOB is participating in the SJPP Government Guaranteed Scheme Covid-19 (GGS Prihatin) to extend working capital facilities* to SMEs during this challenging phase.

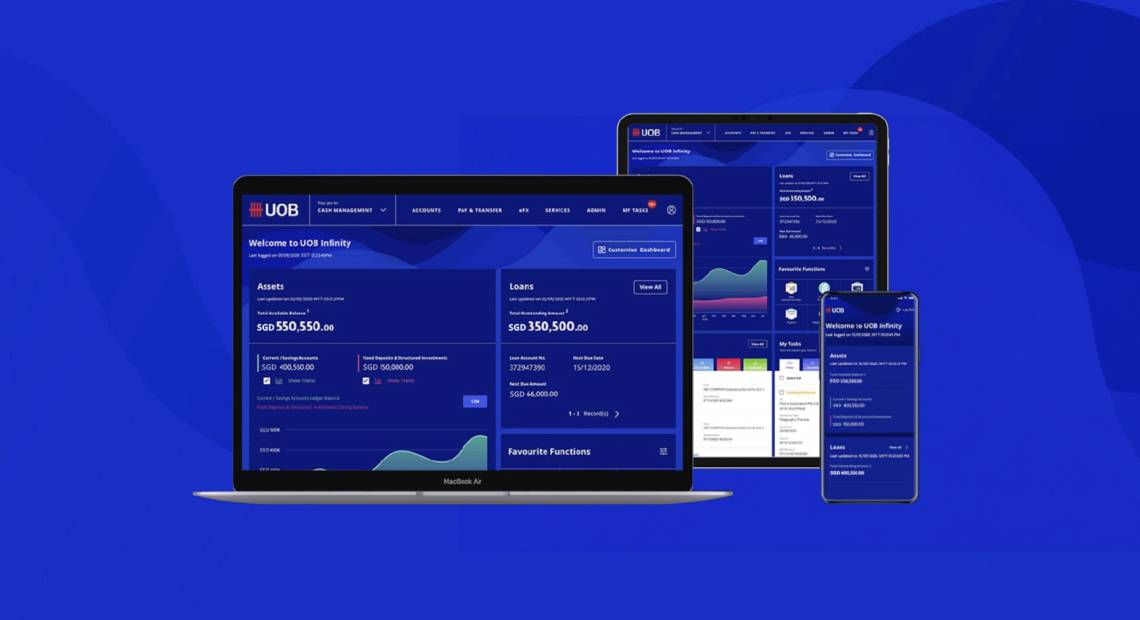

Affected SMEs can apply for this facility through UOB BizSolution and

UOB BizMoney.

*subject to credit assessment

At UOB, we are committed to helping our SME clients make it through this challenging time. And one of the most effective ways we are doing this is by ensuring you have enough cash flow to stay in business.

09 Mar 2026 • 3 mins read

11 Dec 2025 • 3 mins read

23 Oct 2025 • 3 mins read

07 Oct 2025 • 3 mins read