You are now reading:

Why traditional banks are still relevant in the age of digital banking

When you've got big plans for your business, you want a bank you can rely on.

Find out more

Integrates two economies into one ecosystem, unlocking new levels of collaboration

Find out more

Your go-to sustainability guide. Get your customised report today by taking the quiz now.

Take the quizyou are in WHOLESALE BANKING![]()

You are now reading:

Why traditional banks are still relevant in the age of digital banking

Across the region, the banking sector is witnessing a digital revolution. New virtual banks – both local and global – are emerging and attempting to disrupt banking as we know it. This is happening in markets such as China, Hong Kong and Korea. Digital payments in China account for approximately 99 per cent of the country’s non-cash transaction volume and 45 per cent of digital payments worldwide1.

In Malaysia, it is reported that Bank Negara Malaysia plan to issue up to 5 digital banking licenses in 20222. Over the last year, we saw an accelerated move towards online banking because of the need for social distancing, with an increased number of customers switching to digital banking, and the government is encouraging its adoption3. In Singapore, according to a 2020 VISA study on digital banks, 88 per cent of Singapore’s SMEs are open to switching some services to digital banks4.

What do these changes mean for the traditional banking landscape - and most importantly, for the SME customer? We believe that there is space for a healthy co-existence and competition-fuelled innovation. Digital banks, operating solely online, may lack the facilities to provide a one-stop-shop, and may not have sufficient accumulated data, experience and relationships to provide the range of banking services that customers need over their lifetimes5. Traditional banks need to continue to leverage and build upon their distinct advantages to address customer needs.

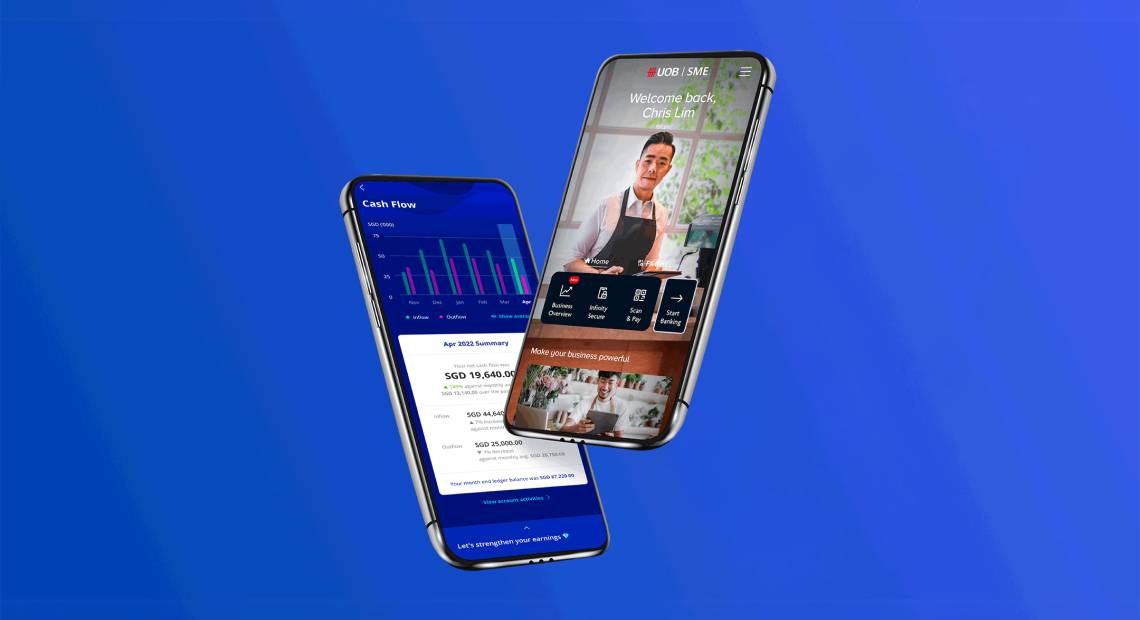

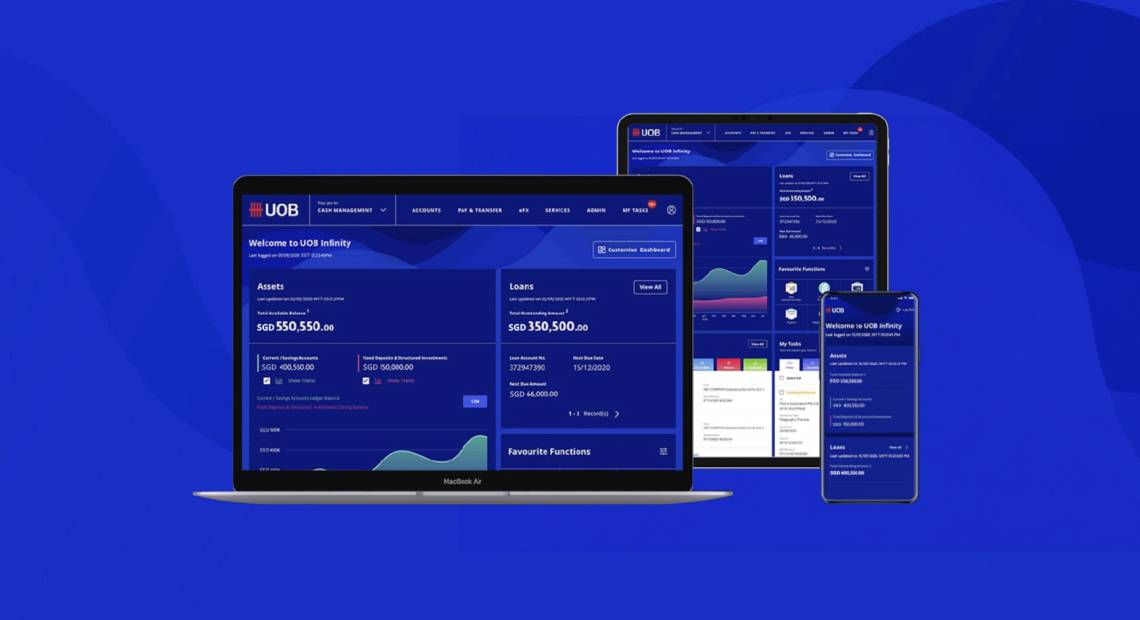

Traditional banks like UOB, being omni-channel, combine several key advantages: they can resolve issues quickly and efficiently, and deliver a more personalised service. These advantages all improve customer loyalty6. A single-channel way of engagement is no longer sufficient, and in Malaysia, our digital solutions are integrated seamlessly with our other touchpoints, delivering an authentic omni-channel experience for our customers.

During the pandemic period, we were able to serve and help our customers without disruption, whether they were visiting branches or conducting their banking needs, such as through our digital and mobile services.

An omni-channel presence is valuable: a study by McKinsey has found that even in digitally advanced European nations, between 30 and 60 per cent of customers prefer doing at least some of their business at branches7.

Furthermore, traditional banks like UOB have built a presence across ASEAN, giving SMEs leverage when looking to venture beyond our shores. Through our regional network, we are able to support the overseas expansion plans of SMEs by allowing them to tap on our resources and in-market expertise.

The importance of building long-term relationships with customers cannot be underestimated. Over the years, traditional banks have a comprehensive understanding and in-depth customer data, enabling them to provide tailored solutions that are relevant to each industry and business. UOB goes beyond banking to help businesses operate more efficiently and, building on its extensive experience, customise solutions and services to suit their specific needs.

The in-depth specialist knowledge and expertise developed over time have also put banks like UOB in an advantageous position.

SMEs value a more personal approach to help them nurture their businesses, especially during a time of crisis. UOB and Dun & Bradstreet spoke with 1,000 SMEs in the region to understand their pain points during the COVID-19 pandemic and what recovery will look like. The recent ASEAN SME Transformation Study 2020 revealed that SMEs want their banks not just to be funding partners, but partners in a journey of transformation, especially during the post-COVID recovery phase.

Traditional banks have strong legacy partnerships and are in a position to create an ecosystem that helps businesses with their digital transformation efforts. According to the same ASEAN SME Transformation Study 2020 mentioned earlier, SMEs want their banks to provide digital solutions support – which we have tapped our partners’ and their services to provide digital solutions such as Beep by StoreHub to help SMEs take their business online to diversify their revenue stream.

In addition to that, UOB Malaysia and The FinLab has also announced the launch of JomX, an initiative to help the Bank’s small- and medium-sized enterprise (SME) customers access a host of digital solutions to accelerate their digitalisation efforts amid COVID-19 challenges. Through the JomX campaign, UOB Malaysia and The FinLab are partnering seven digital solution providers that specialise in digital solutions ranging from business-to-business (B2B) and business-to-customer e-commerce platforms, cloud accounting systems, artificial intelligence and data analytics solutions to robotic process automation, creative technology and marketing technology solutions. The JomX campaign as well as the annual accelerator programme - The Jom Transform Programme also reaffirm UOB’s commitment to helping ensure the viability of our SME customers and the Bank’s continuous effort in supporting our customers during challenging times.

Established banks, like UOB that have built up experience, expertise and relationships over many years are now in a position to pioneer the latest digital technologies to help SMEs navigate the challenging times. Being awarded Singapore’s and Asia’s best bank for SMEs in 2021 is testament that our approach and philosophy is appreciated by the SME business community in the region.

Contact us to learn more about how we can help you with your business needs.

References:

3https://www.nst.com.my/business/2021/02/667027/malaysia-aims-be-regional-leader-digital-economy-2030

4https://fintechnews.sg/44749/virtual-banking/visa-88-of-smes-open-to-switching-to-digital-banks/

5https://www.linkedin.com/pulse/next-challenge-banking-after-millennials-gen-z-marcel-van-oost

09 Mar 2026 • 3 mins read

11 Dec 2025 • 3 mins read

23 Oct 2025 • 3 mins read

07 Oct 2025 • 3 mins read