CARD PRIVILEGES

Tools & Tips

PROPERTY LOAN PROMOTIONS

Featured Solutions

Featured

Guide

Featured Promotion

TMRW made more rewarding

View and redeem your rewards on the UOB TMRW app. Enjoy exclusive deals and UOB coupons in the palm of your hand.

Find out more-

you are in Personal Banking

For Individuals

Wealth BankingPrivilege BankingPrivate BankUOB ReferralFor Companies

Business BankingWholesale BankingForeign Direct InvestmentUOB ASEAN InsightsIndustry InsightsUOB Islamic Banking

Islamic BankingAbout UOB

Corporate ProfileStakeholder RelationsUOB Digitalisation

Economic Outlook

Earlier expectations of moderating growth have now morphed into a more uncertain global outlook.

In the wake of the 2008 Global Financial Crisis, central banks played the crucial role of financial market stabilisers, with loose financial conditions laying the groundwork for an unusually long equity bull market. That is no longer the case now, with central banks currently prioritising the fight against inflation, even with the risk of aggressive rate hikes triggering a recession.

Given the backdrop of high inflation and aggressive monetary policy tightening, we see heightened risks of developed economies such as the US, Eurozone and UK slipping into recession over 2023 as financial conditions tighten while consumer and business confidence declines.

Specifically, we expect a US recession to happen in 1H 2023.

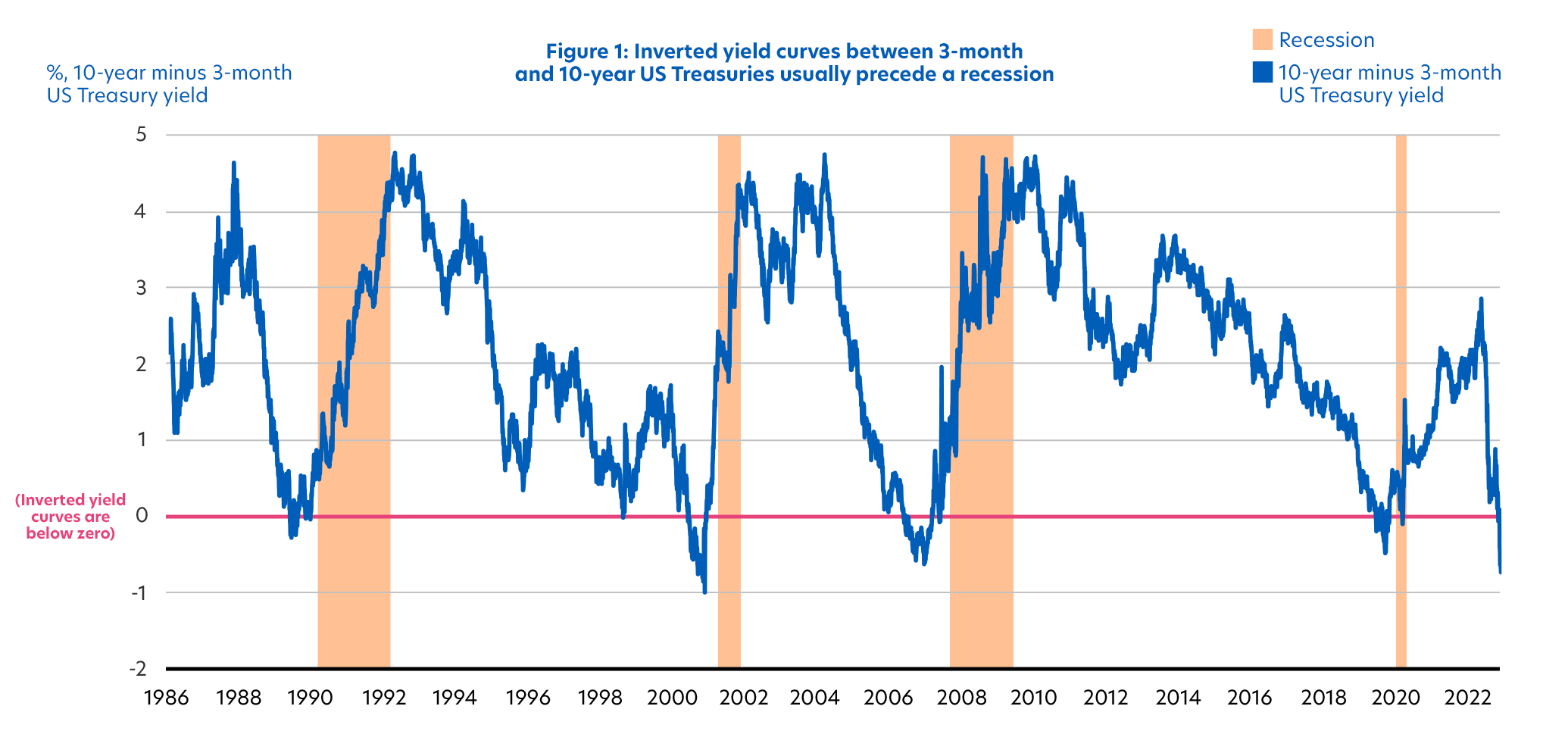

The spread between 3-month and 10-year US Treasury (UST) yields, one of the key indicators highlighted by Federal Reserve (Fed) ![]() Chairman Powell, has also turned negative (inverted) for the first time since March 2020, serving as a recession warning

Chairman Powell, has also turned negative (inverted) for the first time since March 2020, serving as a recession warning ![]() (Figure 1).

(Figure 1).

Source: Macrobond, UOB PFS Investment Strategists (30 November 2022)

On a brighter note, we think any recession will be of the “average” variety, namely short and shallow, assuming the labour market does not weaken drastically and central bank tightening tapers off.

A quicker than expected COVID re-opening in China will also be a positive factor, helping to offset some of the downside risks for the coming year and benefiting the global outlook.

Risks to this base case are escalated geopolitical tensions on the Russia-Ukraine front that fuels another surge in food and energy inflation across the world, US-Sino tensions or a further surge in core inflation that necessitates even higher interest rates to cool demand.

Other risk factors include financial stability risks stemming from tightening financial conditions.

With control of the US Congress now divided, there could also be a paralysis of domestic policies, while we also need to be mindful of a potential US debt ceiling crisis around the middle of the year.

Another potential risk will be complications in China's COVID re-opening, as this could trigger a deeper downturn in global demand and worsen supply chain disruptions.

Emerging Market economies (particularly ASEAN) should outperform, as financial conditions there are expected to remain more benign. Specifically, we expect ASEAN economies to avoid a recession.

Inflation

Our view is that headline inflation![]() and core inflation

and core inflation![]() have likely peaked due to high base effects

have likely peaked due to high base effects![]() , as commodity prices have backed off from their highs, while supply chain disruptions have eased considerably such that the demand and supply relationship adjusts to a new equilibrium.

, as commodity prices have backed off from their highs, while supply chain disruptions have eased considerably such that the demand and supply relationship adjusts to a new equilibrium.

Even so, there is a worry stemming from persistently elevated core inflation, driven by higher costs of services and higher wages.

This elevated core inflation will be the key factor keeping central bankers awake at night, which also means interest rates will remain high for a while.

Risks to inflation remain on the upside, as we are mindful of potential price shocks arising from labour-employer tensions, a new round of higher global energy prices, and renewed disruptions in supply chains.

As such, we are unlikely to see inflation ease back to the 2% level that central banks target.

Central Bank Policies

This is the million-dollar question to which everyone hopes for an answer.

In the near-term at least, more monetary policy tightening looks likely from the major central banks to tame inflation.

Most importantly, we expect the Fed to deliver another 50 basis points (bps) rate hike in February, followed by a 25bps rate hike in March to bring the Fed Funds Target Rate (FFTR)![]() up to 5.00% - 5.25% by the end of 1Q 2023. Thereafter, we expect a pause to the rate hike cycle for the rest of 2023.

up to 5.00% - 5.25% by the end of 1Q 2023. Thereafter, we expect a pause to the rate hike cycle for the rest of 2023.

The Fed’s moves will likely affect what other central banks do, with the exceptions being the Bank of Japan (BOJ), which has kept policy unchanged, and the People’s Bank of China (PBoC), which has cut key policy rates.

Interestingly, the idea of a “Fed pivot” has changed dramatically over the past few months, akin to the repeated shifting of central banks’ goal posts. The “Fed pivot” was once used to signal a reversal to rate cuts sometime in 2H 2023, before it became a policy pause instead. Now, the idea of a “pivot” is smaller rate hikes.

With the Fed having shifted down to a 50bps rate hike rather than 75bps increments, the pace of tightening is slowing, suggesting we are closer to the end, rather than the middle, of the rate hike cycle. This is particularly so for Emerging Market central banks, which started their policy tightening much earlier at the tail-end of 2021.

Asset Class Views

Equities

Given recessionary risks for the year ahead and downside risks for corporate earnings, equities will likely continue to face headwinds in the near term.

As such, we retain a neutral allocation to equities.

Still, stock market valuations have become attractive following the sharp sell-down (Figure 2), and there are pockets of opportunities in quality growth companies, although we caution against chasing short-term stock market rebounds.

-

Forward Price-Earnings Ratio

-

US

-

Europe

-

Japan

-

Asia ex-Japan

| Forward Price-Earnings Ratio | US | Europe | Japan | Asia ex-Japan |

| 10-year Average | 18.4x | 15.5x | 17.8x | 13.4x |

| End-2021 | 22.7x | 16.5x | 17.7x | 15.2x |

| Current | 18.5x | 12.3x | 15.3x | 13.2x |

| Forward Price-Earnings Ratio |

| 10-year Average |

| End-2021 |

| Current |

Source: Bloomberg (30 November 2022)

Fixed Income

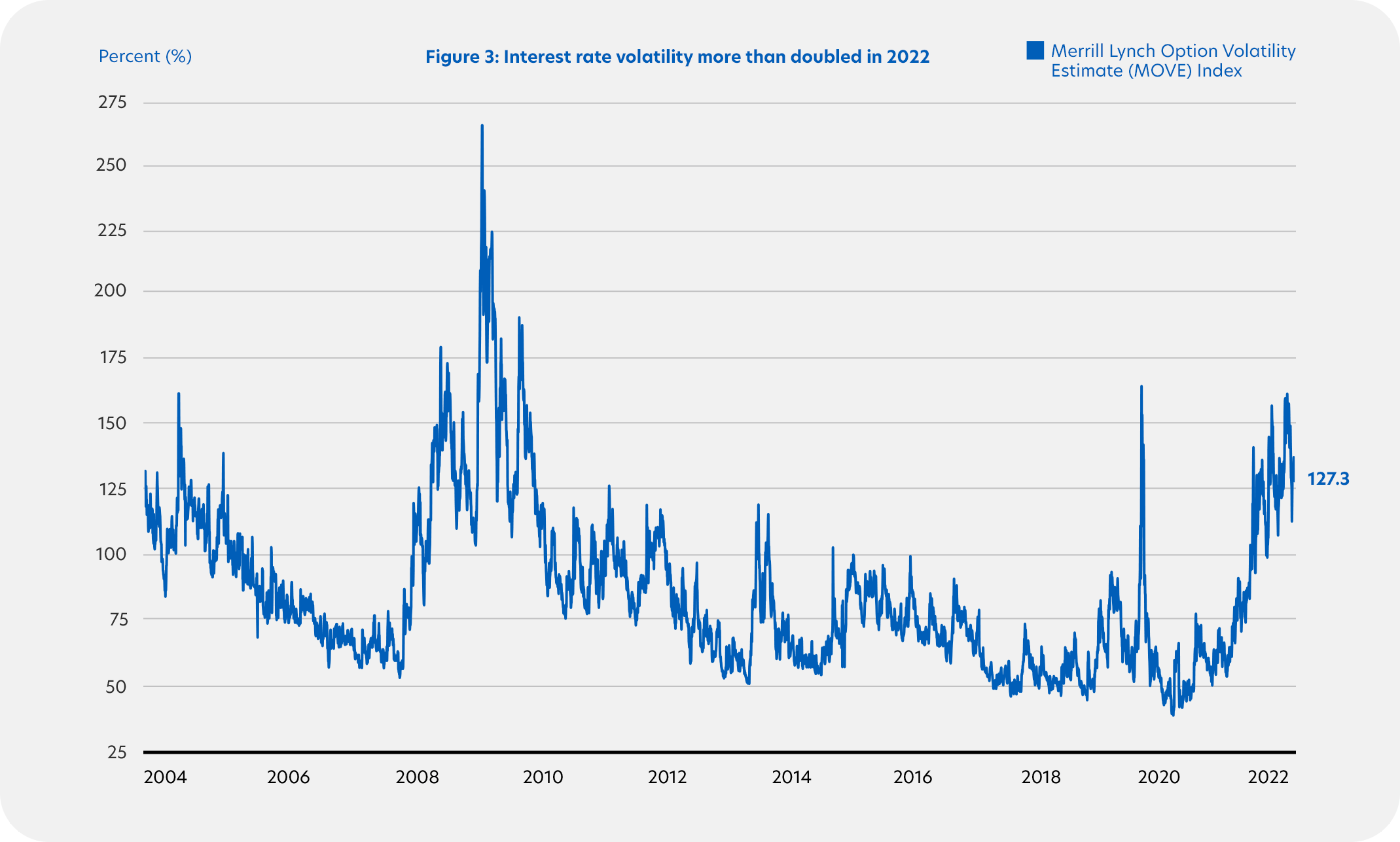

2022 was notable for the unexpected volatility in rates. As a reference, 10-year United States Treasury (UST) bond yields surged by as much as 282 bps, while the MOVE Index![]() , a measure of interest rate volatility, more than doubled from 77 in end-2021 to a peak of 160 in October (Figure 3).

, a measure of interest rate volatility, more than doubled from 77 in end-2021 to a peak of 160 in October (Figure 3).

Source: Macrobond, UOB PFS Investment Strategists (30 November 2022)

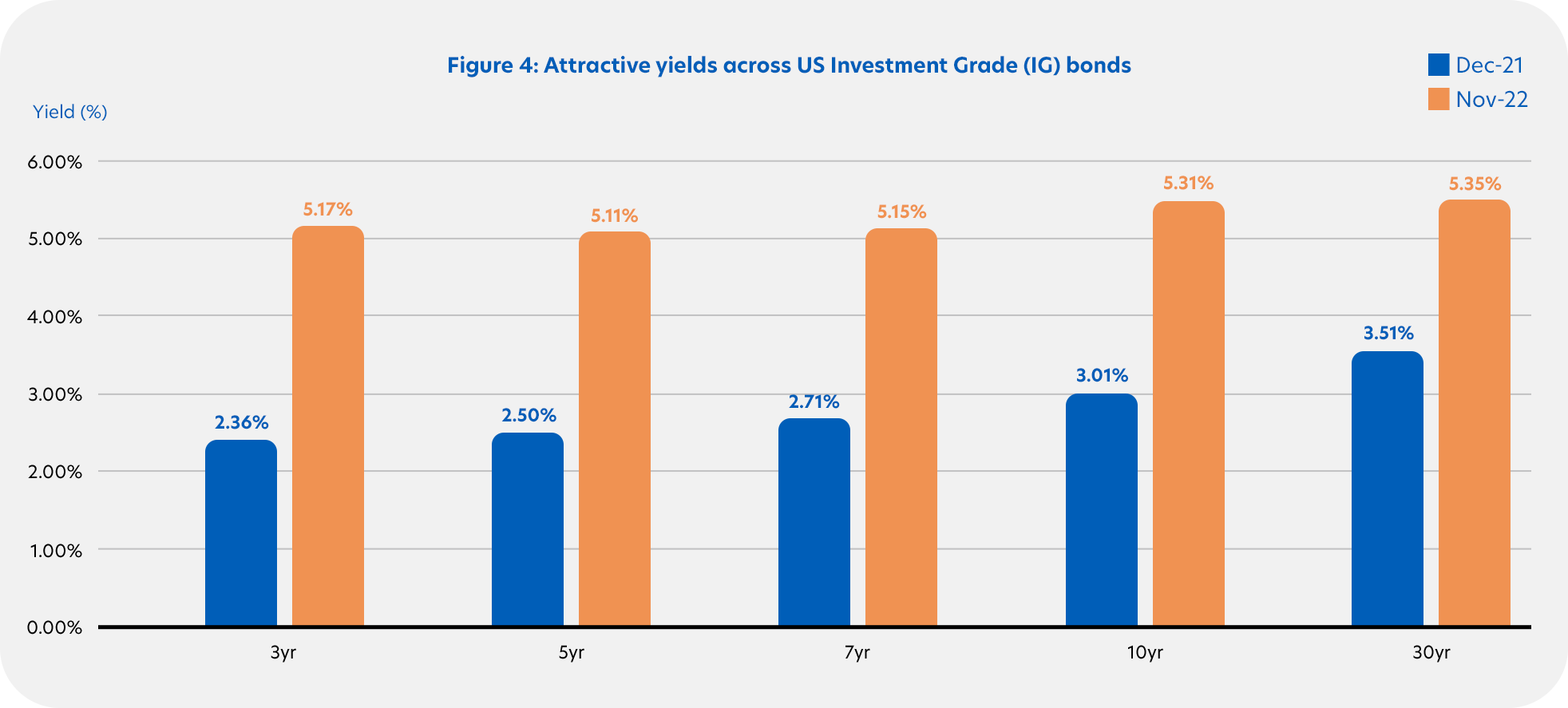

As a result of aggressive central bank rate hikes, even the most liquid parts of the fixed income market such as USTs and sovereign bonds faced a big sell-off. Even so, we believe government bond yields are close to peaking. This is because growth, inflation, and central bank tightening are expected to slow ahead. Given this backdrop, investors need not look beyond Investment Grade corporate bonds to enjoy attractive income, as yields have increased dramatically over the past year to above 5% (Figure 4).

Source: Bloomberg, using the benchmark of the J.P. Morgan US High Grade index (30 November 2022).

If a recession pans out, investors can also benefit from potential capital appreciation from a flight to safe havens. Sovereign bonds and high-quality corporate bonds are defensive assets that can protect portfolios during an economic slowdown or recession.

The takeaway here is that yields for fixed income assets, including government and Investment Grade bonds are now attractive, when considering valuations and potential economic developments. With central bank tightening set to slow ahead, we expect to see bond yields drift lower across 2023.

As such, investors should look to lock in attractive yields and focus on cash flow returns over the coming years.

We however remain cautious on High-Yield corporate bonds as they could remain under pressure if economic activity slows, corporate profitability declines, refinancing costs rise, and default risks increase. This will be magnified for companies that are highly leveraged and with weak balance sheets.

Foreign Exchange and Commodities

After the relentless and broad-based rally in 2022, US dollar (USD) strength will likely normalise in 2023. This comes as the Fed slows its rate hike pace and potentially pause their policy tightening cycle, which suggests we could see the USD normalise to lower levels.

Overall, we think the USD will likely peak in 1Q 2023, in line with our projection of the FFTR topping out then (Figure 7).

When this happens, pressure on Emerging Market currencies should start to abate. However, it is still too early to signal the all-clear given uncertainty over China’s economy, spill-over effects from a recession in the US, UK and EU, and geopolitical tensions.

The outlier risk is that if geopolitical tensions spike over the coming year, any USD downside may be limited, as the greenback will subsequently benefit from safe haven demand.

Commodity prices require a consumption recovery in China. If China’s COVID re-opening is slower than expected or faces unexpected complications, commodities will likely remain under downside pressure. But if China's COVID re-opening proceeds more smoothly than expected, this should unleash pent-up demand and trigger a production recovery, providing support to commodities.

We remain confident in Gold as a portfolio diversifier of risk and a long-term safe haven asset, and a meaningful recovery may start once the FFTR peaks after 1Q 2023.

For crude oil prices, there are contrasting factors in play, with OPEC+ production cuts offset by falling demand and weakening global economic growth.

Country Focus

US

2023 2023 |

|

| GDP (y/y %) | -0.5% |

| CPI (y/y %) | 3.0% |

Equities

US equities may see further downward pressure in 1H 2023 as the economy is likely to enter a shallow recession. A broad-based V-shaped market recovery is not expected. Focus on quality growth stocks and defensive sectors amid higher interest rates.

Fixed Income

With the Fed expected to keep interest rates higher for longer, the 10-year UST yield is expected to hit 4.20% in 1Q 2023, before falling to 3.70% by year-end.

Currency

The US dollar index (DXY) is likely to peak alongside US rates at 109.0 by 1Q 2023, and weaken gradually to 102.0 by end-2023.

Eurozone

2023 2023 |

|

| GDP (y/y %) | -0.5% |

| CPI (y/y %) | 5.6% |

Equities

The Eurozone could fall into a recession in 2023. Stay cautious on equities although valuations are attractive. Heavy energy reliance on Russia remains a long-term risk for the region. European Industrials are a silver lining across the equity markets.

Fixed Income

Following a cumulative 250bps hike in 2022, the European Central Bank (ECB) could raise its refinancing rate by another 25bps to 2.75% in 1Q 2023. Rates are expected to stay high for the entire year thereafter.

Currency

The EUR is expected to bottom at 1.01 against the US dollar (USD) by 1Q 2023, and recover subsequently to 1.08 by end-2023.

Japan

2023 2023 |

|

| GDP (y/y %) | 1.0% |

| CPI (y/y %) | 2.8% |

Equities

The reopening of its borders in 4Q 2022 will continue to benefit reopening-related stocks despite rising recessionary concerns. Japanese Financials might benefit from expectations of changes in monetary policy and higher yields going forward.

Fixed Income

The BOJ is likely to keep its ultra-loose monetary policy, at least until 1Q 2023. That said, Yield Curve Control (YCC)![]() remains in place too.

remains in place too.

Currency

An easy monetary policy stance will push the Japanese Yen (JPY) weaker to 142 against the USD by 1Q 2023, before strengthening slightly to 132 by end-2023 as US rates start to peak.

China

2023 2023 |

|

| GDP (y/y %) | 5.2% |

| CPI (y/y %) | 2.8% |

Equities

The Chinese government’s abrupt shift away from the zero-COVID strategy and policy support for the property sector have boosted market sentiment, skewing equity market expectations towards the upside. What comes after needs to be watched closely, for example, policies stimulating economic growth, the COVID situation, earnings growth recovery, or relief from ADR![]() delisting risk.

delisting risk.

Fixed Income

Relatively weak economic growth will be supported by easy monetary policy which benefits the bond market. Avoid highly leveraged property companies and focus on Investment Grade bonds.

Currency

A weak economy together with accommodative policy are putting pressure on the Chinese Yuan (CNY), with the CNY expected to weaken further to 7.30 against the USD by end-2023.

Singapore

2023 2023 |

|

| GDP (y/y %) | 0.7% |

| CPI (y/y %) | 5.0% |

Equities

Advantages of the Singapore equities market include its resilience and exposure to sectors that historically do well in this part of the market cycle and inflationary phase. In addition, Singapore is a relatively defensive market within ASEAN, and its stability is a key draw for many investors. Focus on regional and global economic reopening-related stocks, Financials and Real Estate Investment Trusts (REITs).

Fixed Income

Singapore bond yields could move further upwards in 1Q 2023 but drift lower across 2023 as US rates peak in 1Q 2023, together with a flight to safe havens amid slowing economic growth. The 10-year Singapore government bond yield is expected to reach 3.30% by end-2023.

Currency

The Singapore Dollar (SGD) is expected to stay strong against its Asian peers as the Monetary Authority of Singapore (MAS) could tighten further, but the SGD is still expected to lag against the USD amid a weakening CNY. The SGD will gradually weaken to 1.40 against the USD by end-2023.

Malaysia

2023 2023 |

|

| GDP (y/y %) | 4.0% |

| CPI (y/y %) | 2.8% |

Equities

Malaysian Financials are expected to be key beneficiaries of rising interest rates as net interest margins (NIMs) expand. Meanwhile, continued regional reopening may provide a suitable environment for commodity and consumer-linked equities to gain favour.

Fixed Income

Malaysian Government Securities (MGS) yields have largely reflected tighter policy. Volatility will likely persist but given already elevated yields, a gradual bull flattening![]() of the yield curve may arise in 2023.

of the yield curve may arise in 2023.

Currency

The Malaysian Ringgit (MYR) is expected to stay weak due to the high correlation with the CNY, while the return of confidence in Malaysia’s markets post-election remains to be seen. The Ringgit is expected to reach 4.65 against the USD by end-2023.

Thailand

2023 2023 |

|

| GDP (y/y %) | 3.7% |

| CPI (y/y %) | 2.7% |

Equities

Stock valuations in the Thailand market remain attractive on the back of continued global reopening and a recovery in domestic spending. Focus on Retail, Healthcare, and Tourism-related sectors.

Fixed Income

The Bank of Thailand (BOT) is expected to adopt a gradual pace of policy tightening to support the economic recovery, with another two 25bps rate hikes to 1.75% expected in 1Q 2023. Therefore, a flattening yield curve is likely to persist throughout 2023.

Currency

The Thai Baht (THB) will remain under pressure amid the uncertain global environment but is likely to outperform its Asian peers on a relative basis due to tourism recovery. It is expected to weaken to 36.2 against the USD by end-2023.

Indonesia

2023 2023 |

|

| GDP (y/y %) | 4.9% |

| CPI (y/y %) | 4.0% |

Equities

Earnings growth excluding the Coal sector is expected to remain healthy. The Banking sector should continue to benefit from economic recovery and steady loan growth, while the Consumer sector will benefit from election campaign activities.

Fixed Income

Even though inflationary pressure is likely to ease as the economy slows, Bank Indonesia is expected to continue raising rates to 6.00% by 1Q 2023 to maintain a reasonable spread with the US.

Currency

The Indonesian Rupiah (IDR) is expected to remain weak and volatile amid heightened external risks such as recession in Western economies and a China slowdown. It is expected to reach 16,200 against the USD by end-2023.

Economic Forecasts

Figure 5: Forecasts for 2023

| US | Eurozone | UK | Japan | Emerging Markets | Asia ex-Japan | China | India | Singapore | |

| 2022 GDP Growth Forecasts | +1.6% | +3.1% | +4.4% | +1.5% | +3.6% | +4.0% | +2.8% | +7.0% | +3.5% |

| 2023 GDP Growth Forecasts | -0.5% | -0.5% | -0.5% | +1.0% | +3.6% | +4.7% | +5.2% | +6.5% | +0.7% |

| Unemployment Rate Projections by the end of 2023 | 4.5% | 7.0% | 4.4% | 2.9% | 5.2% | 2.3% | |||

| 2023 Fiscal Balance Projections Note: Negative implies deficit |

-4.0% | -3.5% | -5.2% | -6.0% | -5.5% | -5.5% | +0.8% | ||

| 2023 Inflation Forecasts | +3.0% | +5.6% | +7.0% | +2.8% | +3.6% (Emerging Asia) +19.4% (Emerging Europe) +11.4% (Latin America) |

+2.8% | +6.1% | +5.0% | |

| 2023 Full-Year Earnings Growth Forecast (EPS) | S&P 500 | MSCI Europe | MSCI UK | MSCI Japan | MSCI Emerging Markets | MSCI Asia ex-Japan | MISCI China | MSCI India | MSCI Singapore |

| +7.0% | +1.6% | -2.0% | +1.8% | +0.7% | +5.3% | +13.4% | +23.7% | +20.0% | |

| Russell 2000 | EuroStoxx 600 | FTSE 100 | TOPIX | CSI 300 | Sensex | Straits Times Index | |||

| +16.4% | +2.1% | -2.0% | +3.0% | +17.6% | +17.4% | +11.6% | |||

| 1-Year Forward Price-Earnings Ratio (P/E) | S&P 500 | MSCI Europe | MSCI UK | MSCI Japan | MSCI Emerging Markets | MSCI Asia ex-Japan | MISCI China | MSCI India | MSCI Singapore |

| 17.7x | 12.3x | 10.0x | 12.6x | 11.7x | 12.8x | 10.4x | 22.2x | 13.4x | |

| Russell 2000 | EuroStoxx 600 | FTSE 100 | TOPIX | CSI 300 | Sensex | Straits Times Index | |||

| 21.0x | 12.3x | 10.0x | 12.2x | 11.4x | 20.6x | 10.9x |

Sources: UOB Global Economics and Markets Research (December 2022), Bloomberg (30 November 2022), IMF World Economic Outlook (October 2022).

Additional Resources

Credits

Credits

Managing Editor

- Winston Lim, CFA

Singapore and Regional Head,

Deposits and Wealth Management

Personal Financial Services

Editorial Team

- Abel Lim

Head of Wealth Management Advisory and Strategy,

Deposits and Wealth Management,

Personal Financial Services

Editorial Team (cont’d)

- Tan Jian Hui

Wealth Management Advisory,

Deposits and Wealth Management,

Personal Financial Services - Low Xian Li

Wealth Management Advisory,

Deposits and Wealth Management,

Personal Financial Services - Zack Tang

Wealth Management Advisory,

Deposits and Wealth Management,

Personal Financial Services

Important notice and disclaimers

The information contained in this publication is given on a general basis without obligation and is strictly for information purposes only. This publication is not intended to be, and should not be regarded as, an offer, recommendation, solicitation or advice to buy or sell any investment or insurance product and shall not be transmitted, disclosed, copied or relied upon by any person for whatever purpose. Any description of investment or insurance products, if any, is qualified in its entirety by the terms and conditions of the investment or insurance product and if applicable, the prospectus or constituting document of the investment or insurance product. Nothing in this publication constitutes accounting, legal, regulatory, tax, financial or other advice. If in doubt, you should consult your own professional advisers about issues discussed herein.

The information contained in this publication, including any data, projections and underlying assumptions, are based on certain assumptions, management forecasts and analysis of known information and reflects prevailing conditions as of the date of the publication, all of which are subject to change at any time without notice. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, United Overseas Bank (Malaysia) Bhd. (“UOB Malaysia”) and its employees make no representation or warranty of any kind, express, implied or statutory, and shall not be responsible or liable for its completeness or accuracy. As such, UOB Malaysia and its employees accept no liability for any error, inaccuracy, omission or any consequence or any loss/damage howsoever suffered by any person, arising from any reliance by any person on the views expressed or information contained in this publication.

ny opinions, projections and other forward looking statements contained in this publication regarding future events or performance of, including but not limited to, countries, markets or companies are not necessarily indicative of, and may differ from actual events or results. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. Investors may wish to seek advice from an independent financial advisor before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider whether the investment or insurance product in question is suitable for you.

We use cookies in order to provide you with better services on our website. By continuing to browse the site, you agree to our privacy notice and cookie policy.