CARD PRIVILEGES & SERVICES

Tools & Tips

PROPERTY

PROPERTY LOAN PROMOTIONS

TMRW made more rewarding

View and redeem your rewards on the UOB TMRW app. Enjoy exclusive deals and UOB coupons in the palm of your hand.

Find out more-

you are in Personal Banking

For Individuals

Wealth BankingPrivilege BankingPrivate BankUOB ReferralFor Companies

Wholesale BankingForeign Direct InvestmentUOB ASEAN InsightsIndustry InsightsUOB Islamic Banking

Islamic BankingAbout UOB

Corporate ProfileStakeholder RelationsUOB Digitalisation

Foreword

Global markets continue to evolve, shaped by uneven economic recovery and rapid technological progress. Investors today face a landscape where shifting growth patterns, innovation, and policy changes present both challenges and possibilities. Amid this complexity, opportunities often emerge for those who remain disciplined and forward-looking.

In our 1H 2026 Investment Outlook, we share the themes we believe will be most influential in the months ahead. We also outline how a diversified and selective approach can help portfolios capture growth while maintaining resilience against potential shifts.

This is also an opportune time to review your investment strategy and ensure it remains aligned with your long-term objectives. I encourage you to speak with your Relationship Managers and Client Advisors for tailored guidance on positioning your portfolio for the evolving environment.

We hope these insights guide your investment journey and reinforce our shared focus on long-term success. Thank you for your continued trust. We look forward to partnering with you in 2026.[ MOY 2026 ]

Dr Neo Teng Hwee

Chief Investment Officer and

Head of Investment Products and Solutions

UOB Private Bank

Overview

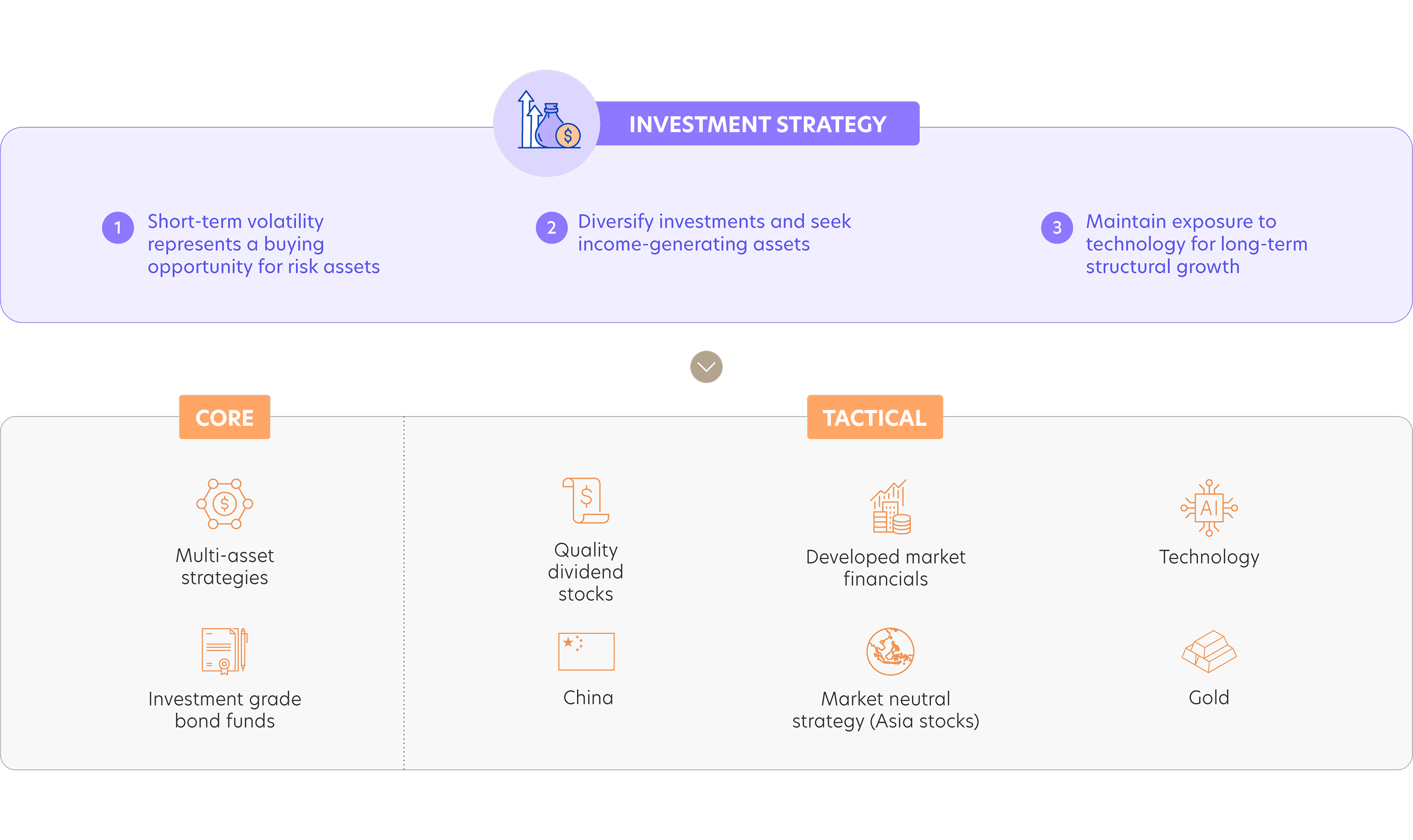

Key themes to watch

A K-shaped economy

The US economy remains distinctly K-shaped, marked by a divergence between booming corporate profits and AI-linked capital expenditure on one hand, and persistent weakness in lower-wage segments on the other.

This environment favours extending the maturities within a bond portfolio and focusing on sectors resilient to uneven demand, such as AI infrastructure and niche consumer plays, while avoiding companies that are affected by global trade tariffs or dependent on lower-income spending.

AI: From digital to physical

AI continues to dominate headlines, but the narrative is shifting from hype to monetisation. The most compelling opportunities lie in bottlenecks such as AI chips, high-bandwidth memory and power infrastructure, where supply remains tight. Beyond software, AI’s next phase is “Physical Intelligence,” embedding cognition into the real world through frictionless interfaces, autonomous systems and mobility solutions.

Going global: Emerging Market (China) and Singapore

Global diversification remains critical as competitive dynamics evolve. China’s ascent as a manufacturing and innovation hub is underscored by its growing Fortune Global 500 presence and leadership in sectors like electric vehicles and telecoms.

Meanwhile, Singapore equities should also benefit from governance reforms and global monetary easing. Sectors investors should keep an eye on are banks, REITs and industrials.

Additional Resources

Contact a UOB Advisor

Download a digital copy

Get more investment insights

We use cookies in order to provide you with better services on our website. By continuing to browse the site, you agree to our privacy notice and cookie policy.