Introduction

PRUMillion Med Active and PRUMillion Med 2.0 are optional medical riders attachable to a regular premium investment-linked insurance plan. These riders are comprehensive medical plans with high annual limits and no lifetime limit. They are designed with their own unique propositions to suit your lifestyle and protection needs.

| PRUMillion Med Active Be in Control. Pay less when you claim less. |

PRUMillion Med 2.0 Be at Ease. High annual coverage with no lifetime limit. |

|

| Discount upon policy inception | ✔ Up to 15% off your medical insurance charges |

✘ |

| Active Pricing | ✔ Premiums will be based on previous claims made. |

✘ |

You can further enhance your medical protection by adding on Active Booster or PRUMillion Med Booster 2.0 to boost your coverage with increased annual limit1, broader hospitalisation care, coverage on maternity complications and be rewarded with No Claims Benefit for preventive care.

1No annual limit when coinsurance and PRUMillion Med Active with Active Booster are selected.

What is Active Pricing?

Active Pricing is a unique feature of PRUMillion Med Active where a discount or an additional charge will be applied to the Base Level Insurance Charges, subject to the terms and conditions. You will receive discount on the Base Level Insurance Charges from the effective date of the policy and continue to enjoy it as long as no claim is made. You will need to pay temporary additional premiums (“Active Premium”) to cover the higher Insurance Charges when a claim is made and approved, subject to the terms and conditions. The Active Premiums payable (if any) will be 95% allocated into Basic Unit Account of your policy. Any unallocated amount will be used to pay commissions and other expenses of the insurance company. 3.75% of Active Premium will be deducted for commission (payable from unallocated premium).

Please refer to the Product Illustration and policy contract for more details on Active Pricing and its terms and conditions.

How does Active Pricing work?

Sam, an Assistant Manager, aged 40, purchases PRUMillion Med Active medical plan. With Active Pricing, Sam pays less premiums when he claims less. Sam will enjoy a 15% discount on the medical insurance charges, paying only RM367 per month throughout the policy tenure if there are no claims made and approved.

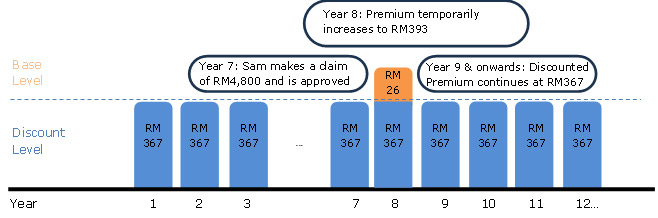

Scenario 1: In the event Sam makes successful claims in Year 7 with less than RM5,000:

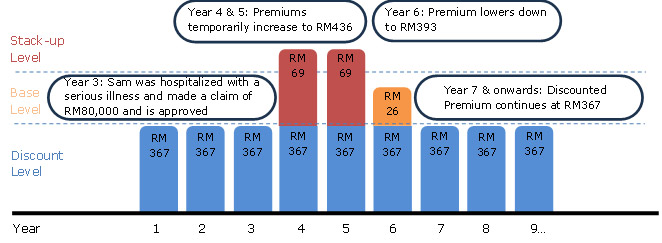

Scenario 2: In the event Sam makes successful claims in Year 3 with RM5,000 or higher:

The scenarios above assume a male, aged 40, non-smoker, occupation class 1 purchases a PRULink Cover policy with Target Sustainability Option of age 80, 100% equity fund, with monthly premium payment through credit card. He selected Basic Sum Assured RM10,000, PRUMillion Med Active R&B200 with deductible of RM500 and Active Booster.

The case scenario is for illustrative purposes only. The diagram shown is not drawn to scale and is intended for illustrative purposes only.